How to fit and use the components model.

Previously

Related posts are:

- A practical introduction to garch modeling

- Variability of garch estimates

- garch estimation on impossibly long series

- Variance targeting in garch estimation

The model

The components model (created by Engle and Lee) generally works better than the more common garch(1,1) model. Some hints about why it is better are in “3 realms of garch modelling”.

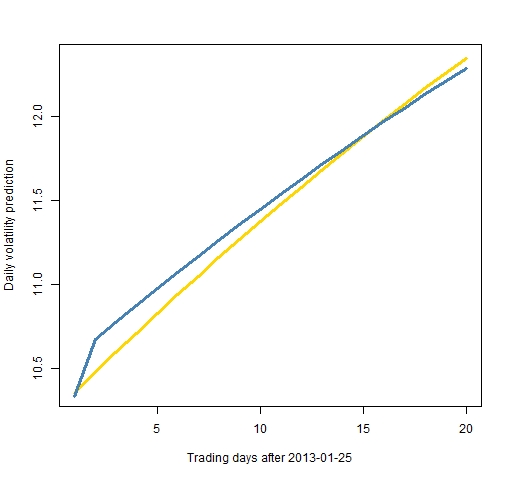

Figure 1 shows predictions of volatility for each day 20 days into the future for two models fit on the S&P 500. The components model has more nuanced predictions of volatility.

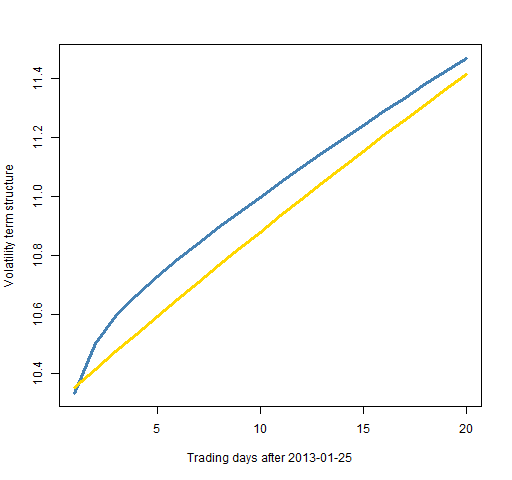

Figure 1: Volatility predictions for each day with the components model (blue) and the garch(1,1) with variance targeting (gold).  It is quite possible that this is not the question you would really like answered. Often what you care about is the average volatility from now until the appointed day. This is sometimes referred to as the term structure — Figure 2 shows this.

It is quite possible that this is not the question you would really like answered. Often what you care about is the average volatility from now until the appointed day. This is sometimes referred to as the term structure — Figure 2 shows this.

Figure 2: Predicted volatility term structure for the S&P 500 using the components model (blue) and the garch(1,1) with variance targeting (gold).  The code to create these plots is shown below.

The code to create these plots is shown below.

R code

The rugarch package allows the option of fitting the components model.

An error

We’ll get to how to do things presently, but first here is a problem I ran into:

> spx.garct <- ugarchfit(comtspec, tail(spxret, 2000))

Error in .hessian2sidedcpp(f, ipars[estidx, 1], arglist = arglist) :

SET_VECTOR_ELT() can only be applied to a 'list', not a 'symbol'

> packageVersion('rugarch')

[1] ‘1.0.16’

I knew what to do after seeing this error because I read the r-sig-finance mailing list. The hypothesis was that changes to Rcpp and relatives probably caused this problem. So updating those packages should do the trick.

> detach(package:Rcpp, unload=TRUE) Error: package ‘Rcpp’ is required by ‘rugarch’ so will not be detached > detach(package:rugarch, unload=TRUE) > detach(package:RcppArmadillo, unload=TRUE) > detach(package:Rcpp, unload=TRUE)

After unloading the packages, I updated the Rcpp and RcppArmadillo packages. Things still didn’t work right, so I did the same exercise of updating numDeriv as well. Then I had different weird behavior.

It turned out there was still a problem with the installation of Rcpp. After installing Rcpp once more, there was success.

If I hadn’t seen the r-sig-finance message with a similar error, then my strategy probably would have included doing a web search on a portion of the error message. In this case the r-sig-finance thread would have shown up.

Onwards

The components model is called "csGARCH" by rugarch and the two extra parameters are called eta11 (ρ in my notation) and eta21 (φ). A specification of it with a t distribution and just a constant mean is:

comtspec <- ugarchspec(mean.model=list( armaOrder=c(0,0)), distribution="std", variance.model=list(model="csGARCH"))

This specification is used like:

> spx.garct <- ugarchfit(comtspec, tail(spxret, 2000)) Warning message: In .makefitmodel(garchmodel = "csGARCH", f = .csgarchLLH, T = T, : NaNs produced

The warning message seems to be about:

> spx.garct@fit$condH [1] NaN

I’m not sure what this is, but I suspect it isn’t a tragedy that we don’t have it.

The estimated coefficients and half-life are:

> coef(spx.garct)

mu omega alpha1 beta1

7.524949e-04 1.245354e-06 2.892064e-08 8.937168e-02

eta11 eta21 shape

9.918261e-01 8.934750e-02 6.010112e+00

> halflife(spx.garct)

Transitory Permanent

0.2870233 84.4534694

Variance targeting seems not to be implemented (yet).

The specification for the garch(1,1) model with variance targeting is:

tvtspec <- ugarchspec(mean.model=list( armaOrder=c(0,0)), distribution="std", variance.model=list(model="sGARCH", variance.targeting=TRUE))

Prediction

Once the models are fit, you can predict.

spx.ctvolfore <- ugarchforecast(spx.garct, n.ahead=20)@forecast$forecasts[[1]][, 'sigma'] * 100 * sqrt(252) spx.tvtvolfore <- ugarchforecast(spx.gartvt, n.ahead=20)@forecast$forecasts[[1]][, 'sigma'] * 100 * sqrt(252)

The structure of the forecast output is not exactly intuitive, but the str function is your friend.

Once we have the predicted volatility in hand, we can plot it. The function to produce Figure 1 is:

function (filename = "dailyvolpred.png")

{

# placed in public domain 2012 by Burns Statistics

if(length(filename)) {

png(file=filename, width=512)

par(mar=c(5,4, 3, 2) + .1)

}

plot(1:20, spx.tvtvolfore, type='l', lwd=3,

col="gold",

xlab="Trading days after 2013-01-25",

ylab="Daily volatility prediction")

lines(1:20, spx.ctvolfore, type='l',

col='steelblue', lwd=3)

if(length(filename)) {

dev.off()

}

}

The function for Figure 2 is:

function (filename = "volpredterm.png")

{

# placed in public domain 2012 by Burns Statistics

if(length(filename)) {

png(file=filename, width=512)

par(mar=c(5,4, 3, 2) + .1)

}

plot(1:20, sqrt(cumsum(spx.ctvolfore^2)/(1:20)),

type='l', lwd=3, col="steelblue",

xlab="Trading days after 2013-01-25",

ylab="Volatility term structure")

lines(1:20, sqrt(cumsum(spx.tvtvolfore^2)/(1:20)),

type='l', col='gold', lwd=3)

if(length(filename)) {

dev.off()

}

}

The value for the mar parameter was intended to be:

c(5, 4, 0, 2) + .1

but somehow escaped notice until I was too lazy to change it.

Hi

I’ve played with rugarch quite a bit, including the component garch model. Generally speaking, the results agree with EViews 7’s estimations.

In my experience, the NaNs problem only shows up with particular series (and not all that often). Why this is so, I don’t know.

Terry,

Thanks for the information.

I had the same problem estimating an sGARCH(2,1). And generally any GARCH of order above (1,1) in variancemodel, so I tried to use 10 years of dayli returns instead of 8.. and that worked. Now I was able to estimate up to an order of (2,2) in the variancemodel but with higher orders same problem reappeared.

This is a typically insightful post on an interesting piece of financial modelling. The mini-tutorial on dealing with obscure R errors however is priceless. Thank you.

Pingback: Changeability of Value at Risk estimators | Portfolio Probe | Generate random portfolios. Fund management software by Burns Statistics

Pingback: Popular posts 2013 October | Portfolio Probe | Generate random portfolios. Fund management software by Burns Statistics

Pingback: garch models caught in the spotlight | Portfolio Probe | Generate random portfolios. Fund management software by Burns Statistics

I don’t get the sqrt(252)

I am running around 520 models with 500 observations in each of the models, using the rugarch package. While all my models are successfully converging some of the have NaN value in CondH. I am not sure if I can safely use that model fits for further analysis? I did try to optimize some of those models in Eviews and Matlab and I was successfully able to do it with any errors. The parameters were also more or less similar. Can you please elaborate more on ConH ?